Global financial stability risks have increased, and the balance of risks is significantly skewed to the downside. Several risks highlighted a few months ago have crystallised, says the latest Global Financial Stability Report from the International Monetary Fund, a multilateral institution.

These include higher-than-anticipated inflationary pressures, a worse-than-expected slowdown in China on the back of COVID-19 outbreaks and lockdowns and additional spillovers from Russia’s invasion of Ukraine, said the report that is used as a baseline scenario predictor for global investing.

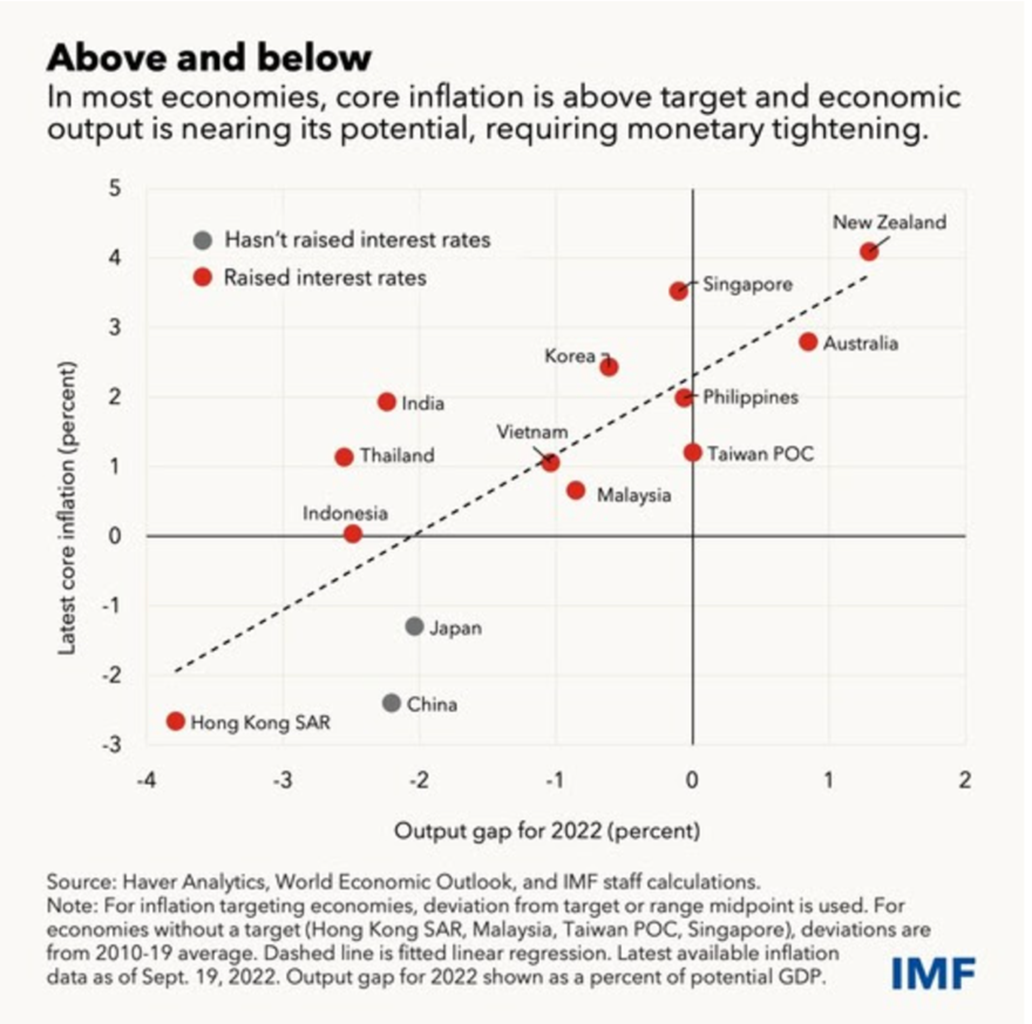

The annual meetings of the World Bank and the IMF last week in Washington DC, bring to light macroeconomic challenges faced by rich, middle income and poor countries. The overall outcome of these conversations presents a worrying picture for middle-income and poorer nations.

Central banks in rich countries have launched a war against inflation. They are raising rates to tame the inflation demon. The World Bank has predicted a recession in 2023. US President Joe Biden predicts a minor recession phase, and Jamie Dimon, chief executive of JP Morgan Chase and a banker the world listens to, predicts a sharp one. There is a broad consensus that American and Western European nations would get away with a minor recession through a phase of austerity. That means governments and businesses would spend less. For now, the employment data in America shows resilience. However, a drop in rich country consumption is bad news for economies dependent on exporting goods and services.

For the year to date, Korea’s benchmark stock index is down 26%, and Taiwan is down 28%. Similar trends are visible in markets like Australia, New Zealand, Malaysia, Thailand and the Philippines. These economies rely on exports. Indonesia and India have stayed buoyant. Indonesia is a net energy exporter and part of the OPEC, the oil-producing nations’ cartel.

Domestic consumption is likely to be the only driver for India’s growth. The World Bank and IMF have cut India’s growth rate below 7%. There are inflationary risks for the economy, and interest rates are likely to slow down the pace of growth. However, lead indicators like monthly GST collection and e-way bills collected for the transport of goods suggest a strong September 2022.

Foreigners have pulled out $23 bn from Indian equities in 2022. In the past, that would have caused harm. When America raised rates in 2013-14, Indian equities tumbled as foreigners pulled money out. This time, Indian shares are holding on to the current levels due to local investors. Domestic institutional investors have injected over $33bn into Indian equities in 2022 so far. There is the hope of a profit growth revival led by the rural and urban consumption demand ahead of the festive season.

However, India cannot remain immune to the world’s woes. Technology services companies rely on spending in rich countries for IT services. The latest results from software companies show satisfactory financial performance but worrying commentary on the situation in Europe. The other factor for IT services companies is the attrition rate. TCS, the most extensive software services Indian company, reported attrition of over 21%, while Infosys announced an attrition rate of 27% for the latest quarter. There is a significant increase in the number of people leaving IT jobs.

Alphaniti can help you identify winners in the Indian stock market. Wondering how to go about it? Here’s where we come in with our platform at www.alphaniti.com to help you take charge of your investments to make investing easy for you!

Thank you for reading this post, don't forget to subscribe!